Specialist tax counsel for your clients considering a charitable trust.

For financial planners, estate planning attorneys, CPAs, and family offices: we collaboratively handle the technical charitable-trust work so you can keep the relationship. Our practice is narrow by design - and intentionally non-competitive with yours.

"Same team, same client. We take the technical charitable trust work off your plate and collaborate with you throughout - the relationship stays yours."

What we cover, and what stays with you.

A clear scope protects the referring relationship. Here's what we take on, and what stays yours - it's the same for everyone, not negotiated case by case.

What we do

Our scope- Charitable trust feasibility, structuring, and modeling (CRT, CLT)

- Annual Form 5227 administration, K-1 distribution, and unitrust calculations

- Major gift consulting - vehicle-agnostic, donor-side modeling

- Personal 1040 preparation for charitably-inclined individuals (limited capacity)

- Coordination with the trustee, custodian, counsel, and the client's CPA on tax-technical questions

What we don't

Your scope- Investment management or asset allocation

- Legal opinions on estate structure, governance, or fiduciary law

- Ongoing general tax work or business returns

- Insurance, annuities, or product placement of any kind

- Solicitation of your client for adjacent services

How a referral typically works.

We're built for clean, collaborative referrals. Most engagements take this shape; we can flex when your client's situation calls for it.

Forming a CRT is a team effort. You keep the client relationship and the broader plan, and the client's CPA keeps theirs. We handle only the charitable-trust piece - scoping the idea, designing the structure, and the specialized trust filings. The attorney drafts the instrument; the trustee and custodian hold and invest.

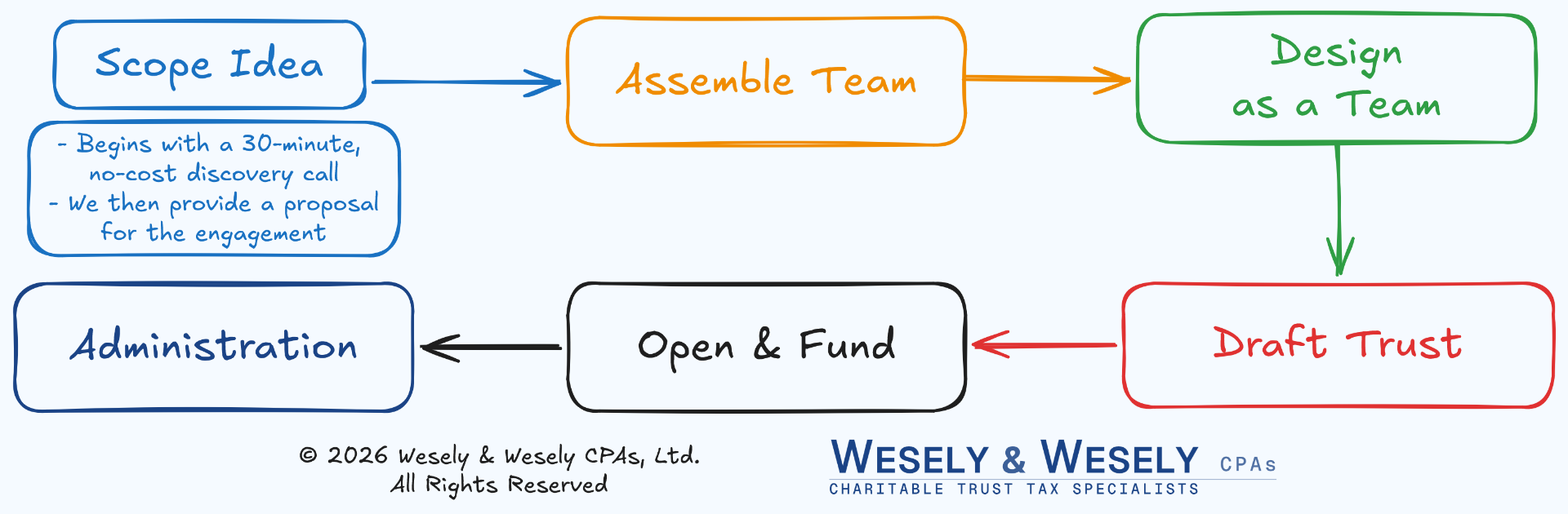

Introduction

You reach out through the contact form, by email, or call. We typically start with a brief feasibility discussion with you, the advisor, before bringing your client into a 30-minute three-way call. The first meeting is no obligation, no fee.

Scope

Within a week of the call, we send a one-page scope memo to both of you. It covers what we'd do, what's out of scope, the timeline, and the fee - agreed up front.

Engagement

If your client signs, we engage. You stay copied on all client communication unless your client requests otherwise.

Next steps

When our scope is complete, your client returns to you for everything beyond the charitable trust work.

The CRT Referral Checklist

The client situations where a charitable remainder trust is worth a closer look, the documents to gather before you call us, and what to expect when we work together. Built to live in your referral file.

Three CRT Strategies Worth Knowing

The tier past the checklist: three situations where a charitable remainder trust does something almost nothing else can - the real-estate flip CRUT, the testamentary stretch-IRA CRT, and the NIMCRUT for income timing - plus the guardrails that decide whether it works.

Three ways to go deeper.

Referral protocol

The full version of how we work with referring advisors - how we communicate, who you'll work with, fee structure, and what you receive at each stage.

Sample engagement

A walkthrough of a typical CRT design engagement, from the introductory call to the final recommendation. Anonymized but representative of the work we deliver.

Spot a CRT candidate

An insight piece: the three signals that tell you a charitable remainder trust is worth a conversation - and how we fit in without taking over your relationship.

What advisors usually ask us.

01Do you take over the client relationship?+

No. We're small and focused on purpose. We handle the charitable-trust piece and collaborate with you; your client comes back to you for everything else. Once the charitable trust is funded, your role doesn't change.

02How do you fit with the existing team - the financial planner, the attorney, the other CPA?+

We work alongside whoever is already at the table and take only the one technical corner we know best. Because we're closest to the charitable trust piece, we often "quarterback" that part - but everyone keeps their lane.

03How do I know if a client is even a candidate?+

Three signals: a large appreciated asset they'd be taxed heavily to sell, desire for an income stream rather than a lump sum, and comfort giving up access to the principal. If you see those line up, it's worth a call - there's a fuller walkthrough in our insight on spotting a CRT candidate.

04What does it cost, and how do referrals work?+

We work on a fixed-fee agreed up front. A referral usually starts with a short intro call - we'll tell you within about thirty minutes whether we're the right fit, and if we're not, we usually know who is.

Educators first.

Teaching other professionals is how we grow, and how the field gets better at spotting a good CRT. A snapshot of where we've been - and where we're headed.

this work

across the firm

combined practice

Recent rooms

- 2025MGPA Annual ConferenceCharitable Tax Planning Under OBBBA · 80 gift planners

- 2025FPA of Minnesota - Ascend ConferenceCRTs in Practice · 130 planners

- 2025MNCPA Tax ConferenceCRT Advanced Strategies · 120 CPAs

- 2026Minnesota CLE Probate and Trust ConferencePanel: Charitable Gift Planning in Practice · 100 attorneys

Upcoming

- 2026FPA of Minnesota - Ascend ConferenceOctober

- 2026MGPA Annual ConferenceOctober

- 2026MNCPA Tax ConferenceNovember

- 2027Red River Estate Planning CouncilThree-hour CLE seminar - January

Between the conferences, we run private education sessions for advisor teams and RIAs year-round.

Have a client with a charitable-trust question?

Start with an introductory call. We'll tell you within thirty minutes whether we're the right fit - and if we're not, we usually know who is.