A typical CRT design engagement, walked through.

Anonymized but representative. Names changed, numbers rounded; everything else reflects how a real engagement actually runs from the introductory call to the final recommendation.

Introductory call

The referring financial planner emails us the high-level: the Andersons, the concentrated UNH position, and what they're trying to accomplish. We reply and agree a CRUT appears to be a great fit and warrants a closer look.

We set up a three-way call with the client to dig into the specifics and agree on next steps: a scope memo within a week, agreed before any billable work begins.

Scope memo

A short memo to both the financial planner and the Andersons. Lists what we'd do, the deliverable, the timeline, and the fee - agreed up front. The Andersons sign within two days.

The scope memo and the engagement letter are separate documents. The scope memo is ours; the engagement letter that follows is processed through our standard intake workflow.

Modeling

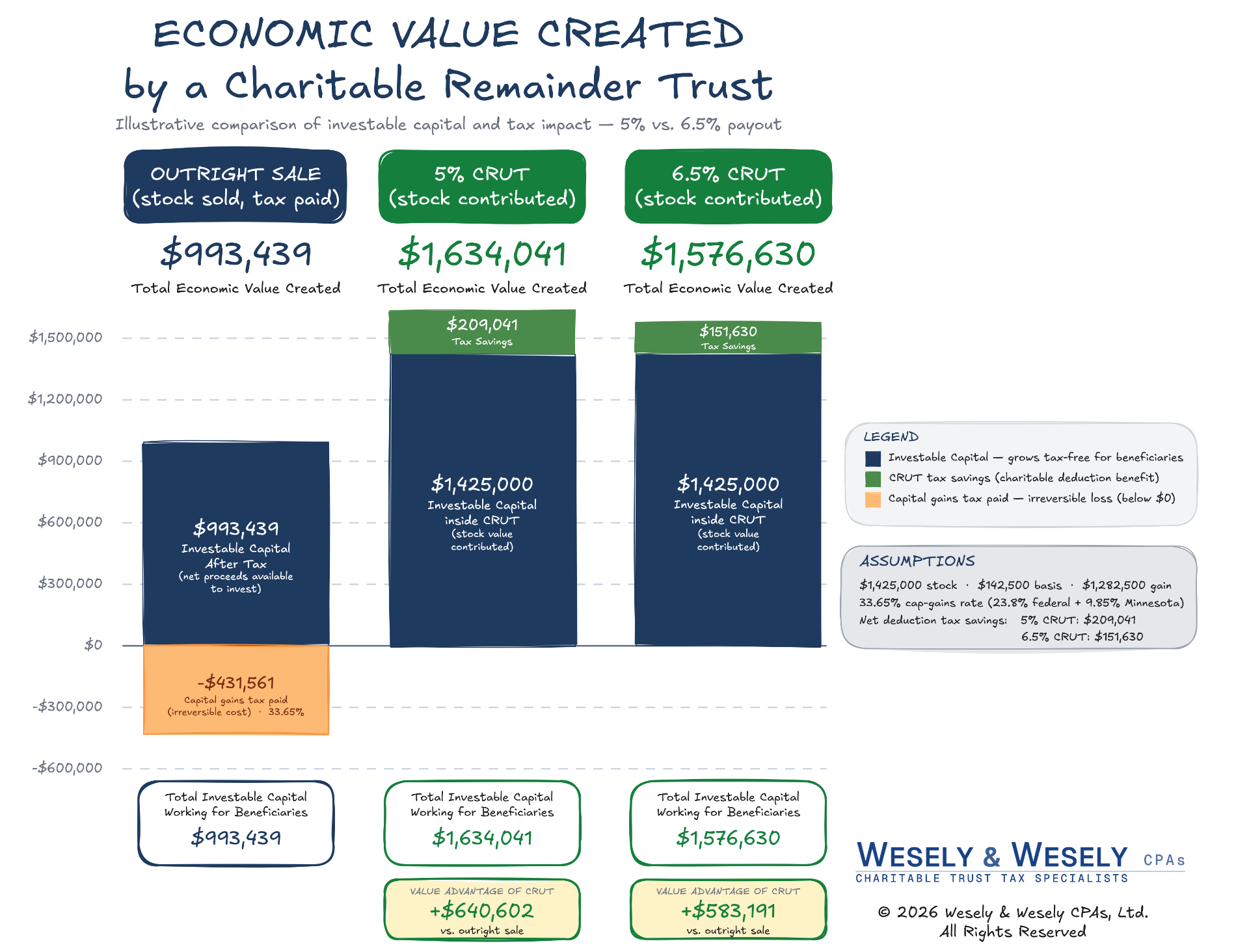

We model three candidates with the Andersons' real numbers: outright sale, and both 5.0% and 6.5% unitrust over the couple's two lives.

For each, we project after-tax income, deduction value, residual to charity, and family wealth retained - across a variety of time horizons. Assumptions are made explicit so the financial planner (and the Andersons) can challenge any of them. Various visual comparisons are provided to clearly illustrate and maximize clarity.

This is a version of one type of comparison we typically share with donors and their advisors. The underlying numbers are run in spreadsheet form for the technical professionals on the team, while the diagram is the version that makes the result understandable in thirty seconds.

Recommendation memo

The recommendation memo lands in the Andersons' inbox and the attorney's inbox at the same time. One preferred structure, two alternatives, and an honest description of what the Andersons give up with each option.

The memo explains what we recommend and why, with supporting schedules. A short caveat at the end notes whether a simpler vehicle would produce more total dollars to charity if income is not actually needed - we've modeled both, and either remains a defensible choice.

Coordinating next steps

If the Andersons proceed, we coordinate with the client's attorney on trust instrument drafting, and initial funding mechanics. Our planning engagement closes; if the Andersons want us to administer the trust going forward, a separate annual engagement begins.

Have an Anderson?

If a client of yours is sitting on an appreciated position and considering diversification strategies, start with an introductory call. We'll tell you within thirty minutes whether the math supports a closer look.